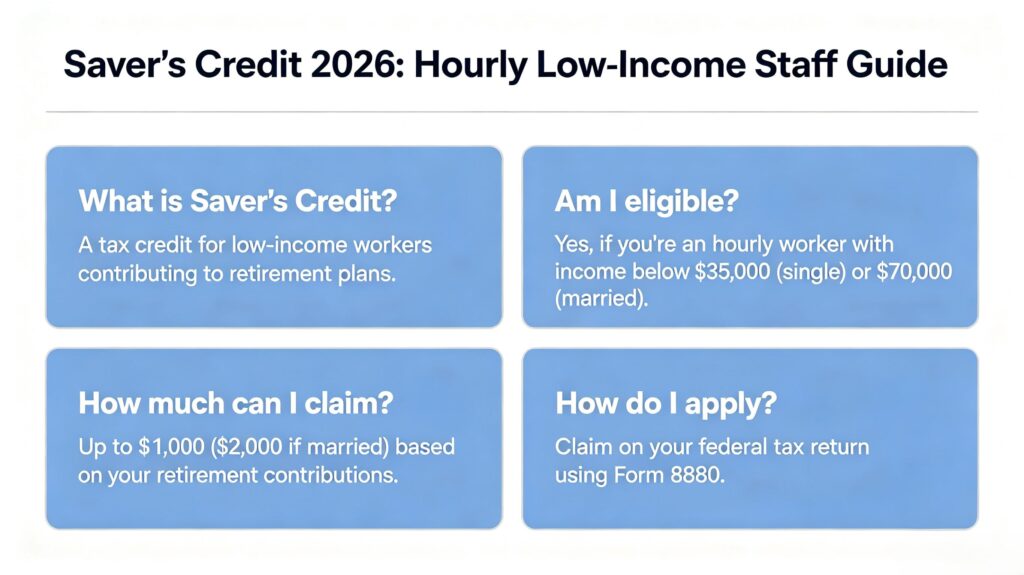

TL;DR: The Saver’s Credit 2026 is a simple hidden IRS tax credit that lets low-wage hourly workers claim up to $1,000 individually and up to $2,000 for joint filers simply by making small retirement account contributions in the 2026 tax year.

Most low-wage hourly workers live on tight monthly budgets.

They prioritize rent payments, grocery shopping, utility bills, and basic daily necessities.

Because every dollar counts, they rarely research lesser-known federal tax benefits.

One of the most underused benefits for working-class Americans is the Saver’s Credit 2026.

Unlike common tax deductions that only reduce your taxable income, this credit lowers your tax bill dollar-for-dollar.

Many eligible hourly, seasonal, part-time, and minimum-wage employees leave hundreds or thousands of dollars unclaimed each year.

🎁 2026 US Savings Tax Rules: How Low-Income Workers Can Boost Savings Easily

🎁 Unclaimed Free Government Cash for Low-Income Workers 2026 (EITC, LIHEAP & Utility Relief)

How the Hidden Saver’s Credit 2026 Benefits Low-Wage Hourly Workers

The official IRS name for this program is the Retirement Savings Contributions Credit.

It was created exclusively to help low and moderate-income Americans build retirement savings without financial strain.

The program rewards workers for voluntarily depositing small amounts into qualified retirement accounts.

Even contributions as low as $500 or $1,000 per year can generate a significant tax reduction.

For hourly workers who cannot afford large retirement investments, this credit is extremely accessible.

The 2026 credit structure follows three fixed percentage tiers: 50%, 20%, and 10%.

Your exact credit percentage depends entirely on your adjusted gross income and filing status.

Lower AGI always qualifies you for a higher credit percentage rate.

Single filers can receive a maximum credit of $1,000.

Married couples filing jointly can receive a combined maximum credit of $2,000 for 2026.

2026 Official AGI Income Limits for Saver’s Credit Qualification

The IRS updated all income brackets for inflation for the 2026 tax filing season.

These thresholds determine whether low-wage hourly workers qualify for the 50%, 20%, or 10% credit tier.

For single filers and head-of-household workers:

50% credit rate: AGI equal to or below $24,500

20% credit rate: AGI between $24,501 and $27,500

10% credit rate: AGI between $27,501 and $37,500

For married couples filing jointly:

50% credit rate: AGI equal to or below $49,000

20% credit rate: AGI between $49,001 and $55,000

10% credit rate: AGI between $55,001 and $75,000

Most retail staff, restaurant hourly employees, warehouse workers, and seasonal laborers fall perfectly within these brackets.

Unfortunately, these worker groups are the least likely to know or file for the Saver’s Credit.

View official IRS annual inflation-adjusted income bracket standards

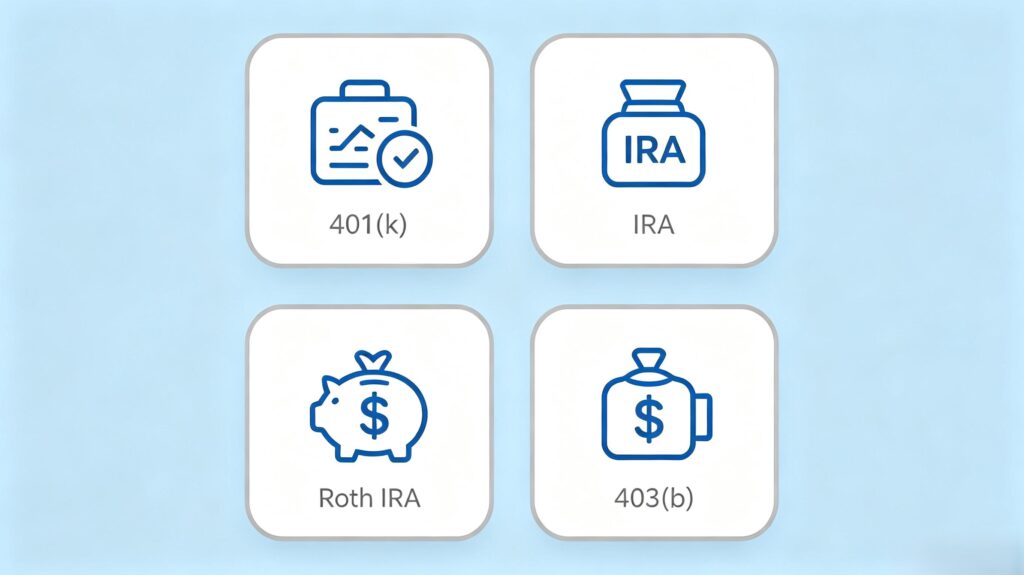

Which Retirement Accounts Qualify for the 2026 Saver’s Credit

Only personal voluntary contributions count toward your credit calculation.

Employer matching funds do not qualify and cannot be added to your contribution total.

Eligible account types include all common retirement plans accessible for low-income workers.

Qualified accounts for 2026 include:

Traditional IRA and Roth IRA personal contributions

401(k) and 403(b) workplace payroll deductions

SIMPLE IRA plans for small-business employees

SEP IRA contributions for self-employed hourly workers

Automatic enrollment retirement plans offered by employers

Official guide to IRA, 401(k) and eligible workplace retirement accounts

You do not need high income or large savings to participate.

Even sporadic small contributions throughout the year will increase your eligible credit amount.

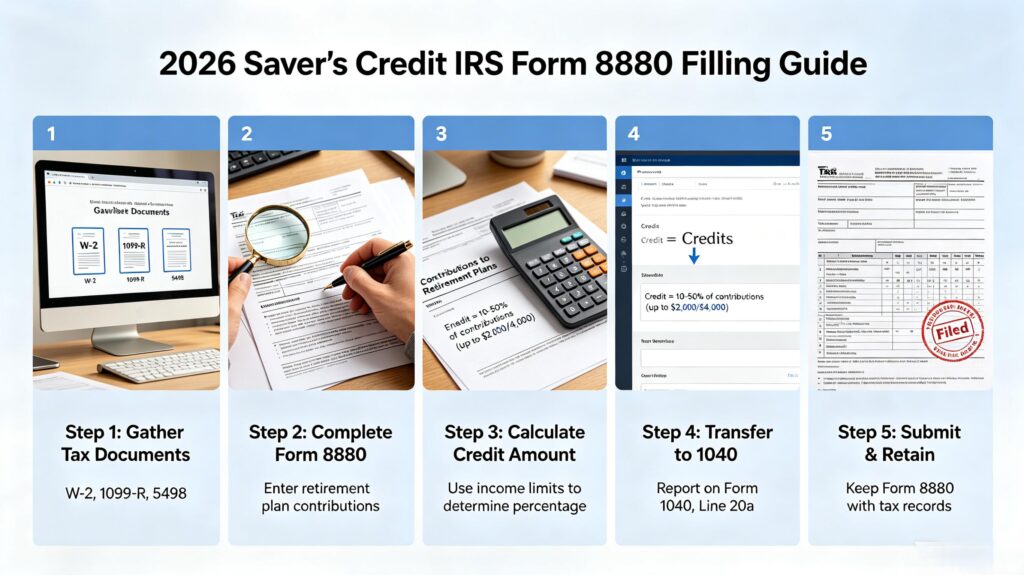

Step-by-Step Process to Claim Saver’s Credit 2026 Using IRS Form 8880

Claiming your retirement tax credit follows a simple official IRS process.

First, calculate every voluntary retirement contribution you made during the 2026 tax year.

Second, confirm your filing status and final adjusted gross income.

Third, match your income to the correct 50%, 20%, or 10% credit tier.

Fourth, complete every section of IRS Form 8880 accurately.

Download printable official IRS Form 8880

Fifth, attach the finished Form 8880 to your federal income tax return.

Sixth, file your taxes before the official IRS annual deadline.

Check the latest federal tax filing deadline from the IRS

The most common mistakes that disqualify workers include miscalculating AGI, adding employer matches, or skipping Form 8880.

Double-checking these simple steps guarantees maximum credit approval for low-wage earners.

Frequently Asked Questions About Saver’s Credit 2026 for Hourly Workers

Who is eligible for the Saver’s Credit 2026?

All low and moderate-income hourly workers, part-time employees, seasonal staff, and self-employed workers qualify if their AGI falls within official IRS 2026 brackets.

Can minimum-wage workers claim the Saver’s Credit?

Yes, minimum-wage hourly employees frequently qualify for the highest 50% credit tier due to low annual AGI.

Is the Saver’s Credit refundable?

The Saver’s Credit is a non-refundable tax credit that directly reduces your federal tax liability dollar-for-dollar.

Do small monthly retirement deposits qualify?

Yes, all voluntary personal contributions, regardless of amount, count toward your 2026 credit calculation.

Final Takeaway

The Saver’s Credit 2026 remains one of the most overlooked federal benefits for low-wage hourly households.

By contributing small amounts to retirement accounts, working-class Americans can reduce taxes and build future financial security.

Understanding official income limits, qualified accounts, and Form 8880 filing steps allows any eligible worker to claim the full $1,000 or $2,000 maximum credit in 2026.

All federal benefit rules, income limits and grant amounts referenced in this article apply exclusively to the 2026 tax and fiscal year.

Policy adjustments may occur at state and federal levels after publication.

We are not licensed tax attorneys, CPAs or official government representatives.

All program eligibility verifications, tax filings and benefit applications must be completed via official .gov federal portals to confirm individual qualification.

Get neutral financial guidance from the official Consumer Financial Protection Bureau

This content is for general educational guidance only and does not constitute official financial, tax or legal advice.

Savelyfi and CalcfincePro accept no liability for financial outcomes resulting from reader self-submitted government benefit claims.