TL;DR simple saver’s credit 2026 guide for low-wage hourly workers breaks down the underused IRS tax credit that lets minimum and low-income employees recover up to $2,000 annually for putting money into retirement accounts. This refundable credit works alongside EITC without cutting your existing federal benefits, and all filing steps rely on free official IRS tools with no third-party fees. This full simple saver’s credit 2026 guide for low-wage hourly workers eliminates all confusing IRS filing hurdles for minimum-wage staff. This all-in-one simple saver’s credit 2026 guide for low-wage hourly workers covers every filing detail you need for maximum tax refunds.

Millions of hourly US workers earn modest wages every year and assume saving for retirement is completely out of reach. Rent hikes, grocery inflation, utility bills and regular daily expenses eat up nearly every dollar of their monthly paycheck. Most mainstream retirement guides target six-figure salaried professionals, ignoring tax incentives built exclusively for low and moderate earners.

This simple saver’s credit 2026 guide for low-wage hourly workers breaks down every eligibility rule overlooked by hourly earners across all US industries. Continue reading this simple saver’s credit 2026 guide for low-wage hourly workers to break down every IRS rule tailored for hourly minimum wage staff.

Few low-wage staff have heard about the Saver’s Credit, officially called the Retirement Savings Contributions Credit. The IRS created this credit to encourage hourly, part-time and seasonal employees to build long-term retirement security without sacrificing essential living costs.

🎁 CalcfincePro Financial Calculation Homepage

Many people mistakenly believe tax breaks for retirement only apply to high earners who can afford large monthly contributions. The Saver’s Credit reverses this dynamic by giving cash back to households with tight annual income limits. Even small monthly deposits into an IRA or workplace 401(k) qualify you for partial or full credit payouts during tax filing season.

IRS Official Saver’s Credit Main Portal

simple saver’s credit 2026 guide for low-wage hourly workers: Eligibility Tiers, Payout Amounts And Income Caps

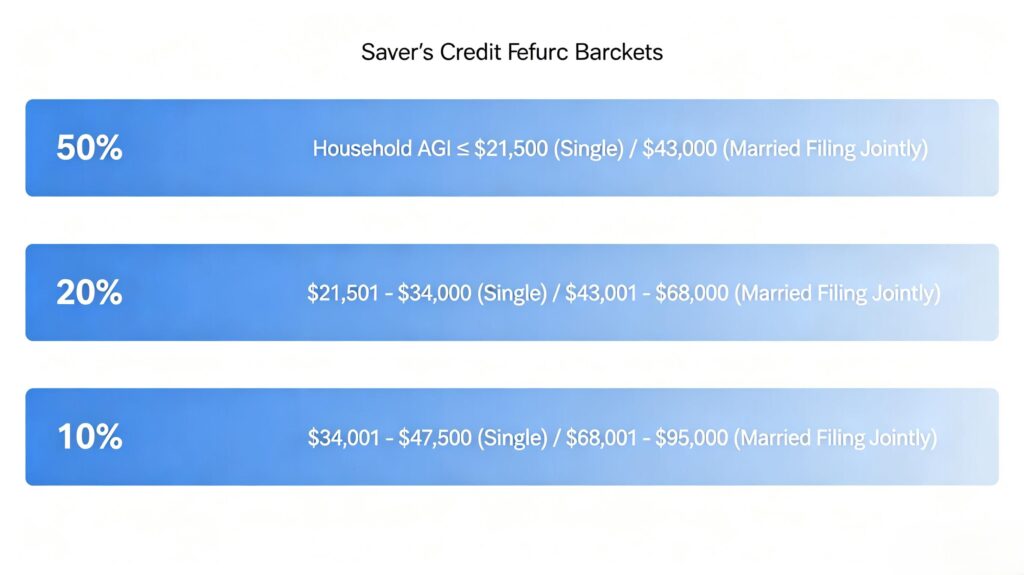

The Saver’s Credit uses three tiered refund percentages based on your total household adjusted gross income, filing status and whether you contribute to qualified retirement accounts in the tax year 2026. Each tier delivers a different portion of your contributions back as a direct tax credit.

Tier one offers a 50% credit rate, the highest possible return for low earners. Single filers qualify for this bracket when their AGI sits below $24,500. Married couples filing jointly can earn up to $49,000 to hit the 50% tier. Heads of household have a $36,750 maximum AGI limit for the top refund rate.

Tier two gives a 20% credit rate for middle-low earners. Single workers with AGI between $24,501 and $27,750 fall here. Joint filers range from $49,001 to $55,500, while head of household limits stretch from $36,751 to $41,625.

Tier three delivers a 10% credit rate, the lowest available bracket. Single filers earn $27,751 to $37,500, joint couples hit $55,501 to $75,000 and household heads qualify with AGI from $41,626 to $56,250. Any income above these upper thresholds removes full eligibility for the Saver’s Credit entirely.

The maximum annual contribution the IRS counts toward this credit is $4,000 for single filers and $8,000 for married joint filers. The highest single-person credit value hits $2,000, calculated as fifty percent of the $4,000 qualifying contribution cap. Couples can receive a combined maximum credit of $4,000 each tax year.

Simple Saver’s Credit 2026 Guide Breakdown For Low-Wage Hourly Workers To Maximize Tax Refunds

Only workers aged 18 or older qualify for the Saver’s Credit. Full-time students, dependents listed on another person’s tax return and minors cannot claim this benefit regardless of retirement contributions made during the year. All qualifying retirement account deposits must come from earned wages, not investment passive income or gift funds.

IRS Topic 610: Saver’s Credit Eligibility Rules

Which Retirement Accounts Count Toward The 2026 Saver’s Credit

The IRS accepts contributions made to several standard retirement savings vehicles for credit calculation purposes. Traditional Individual Retirement Accounts and Roth IRAs both fully qualify, including regular annual deposits and catch-up contributions for people age 50 or older.

Workplace-sponsored plans also meet eligibility rules. 401(k) accounts, 403(b) plans for school and hospital staff, SIMPLE IRAs and SEP IRAs for self-employed hourly workers all count toward your Saver’s Credit calculation. Voluntary after-tax payroll deductions from your employer directly apply to your yearly qualifying contribution total.

Non-qualified investment brokerage accounts, regular savings accounts, certificates of deposit and crypto asset holdings do not count toward the credit. Only official IRS-approved retirement savings structures unlock this tax refund opportunity for low-wage employees.

Step-by-Step Guide To Claim The Saver’s Credit Using IRS Form 8880

Every filer who qualifies for the Retirement Savings Contributions Credit must complete IRS Form 8880 alongside their standard federal tax return. This document calculates your tier percentage, total qualifying contributions and final credit amount automatically once you input household income and retirement deposit figures.

IRS Official Form 8880 Introduction

IRS Form 8880 Official PDF Download

You do not need to purchase paid tax software to fill out and submit Form 8880. The IRS Free File program provides fully guided zero-cost tax preparation tools for all households with AGI under $79,000 per year. The platform auto-populates credit calculations after you enter IRA or workplace retirement contribution amounts from your annual tax forms like W-2, 1099-R and 5498.

IRS Free File Zero-Cost Tax Filing Tool

Follow this simple filing workflow each tax season to capture your full Saver’s Credit value:

- Collect all year-end retirement account tax statements before starting your return.

- Log into IRS Free File and select the filing status matching your household setup.

- Enter total annual earned income from all W-2 hourly jobs.

- Navigate to the retirement credit section and input all qualified IRA or 401(k) deposits.

- The system auto-generates Form 8880 and calculates your tiered refund amount.

- Review your total refund projection, which combines Saver’s Credit with other eligible credits like EITC.

- E-sign and submit your federal return directly through the IRS secure portal at no cost.

IRS News Release: Maximize 2026 Saver’s Credit

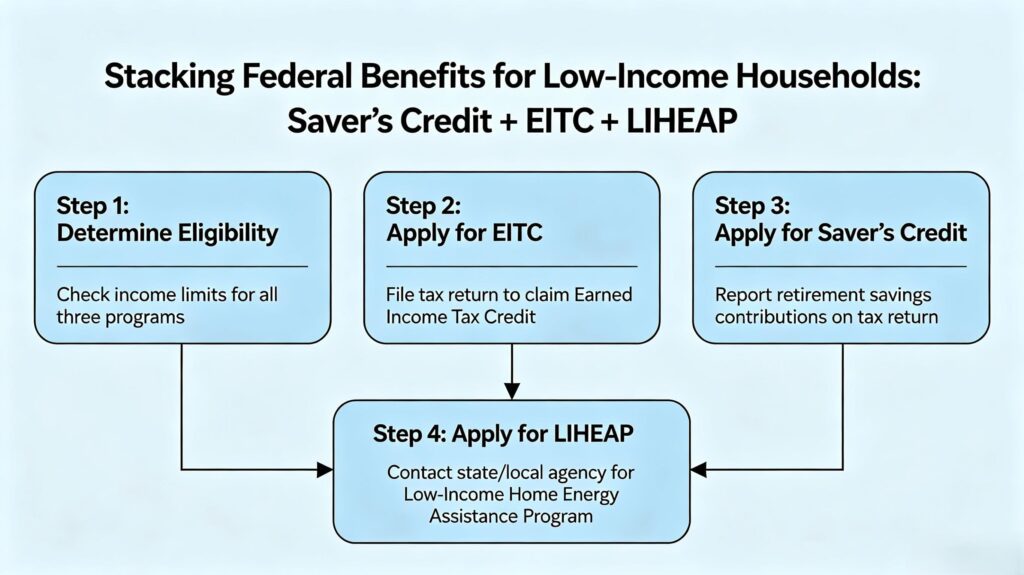

simple saver’s credit 2026 guide for low-wage hourly workers: Stack Saver’s Credit With EITC & Federal Benefits

One major advantage of the Saver’s Credit is its fully stackable design alongside other popular working-family tax support programs. Claiming this retirement incentive does not reduce eligibility or payout values for the Earned Income Tax Credit, Child Tax Credit or dependent care credits.

IRS EITC Official Page (For Stacked Benefit Reference)

Low-income households regularly combine EITC annual refunds with Saver’s Credit payouts to receive thousands of extra dollars during tax filing season. Receiving LIHEAP utility assistance, unclaimed state-held cash assets or DOL recovered unpaid back wages also has zero negative impact on your Saver’s Credit qualification.

🎁 Full Guide to Unclaimed Federal Cash Benefits for Low Earners 2026

State-level benefit programs and local utility relief grants operate under separate income verification systems. Federal tax credits including the Saver’s Credit do not share eligibility databases with HHS energy support initiatives, so dual participation remains completely allowed for all qualifying low-wage households.

HHS Official LIHEAP Energy Grant Program

Unclaimed Forgotten Retirement Assets For Low-Income Former Workers

Many hourly staff leave small balances behind in old workplace 401(k) plans after switching jobs over the years. These dormant retirement accounts become unclaimed assets managed by state treasury departments after multiple years of inactivity. You can search for forgotten retirement funds at the national USAGov unclaimed money portal before filing taxes each year.

Recovering old retirement account balances counts as new contributions toward your Saver’s Credit in the tax year you claim the assets. Combining recovered forgotten savings with new monthly IRA deposits maximizes your qualifying contribution total and pushes your credit value higher.

USAGov National Unclaimed Asset Search

How To Check All Matching Federal Benefit Eligibility In One Place

New and returning low-wage filers can run a full eligibility scan for every available federal credit, grant and cash support program via Benefits.gov. This official national portal asks simple questions about your annual wages, household size, housing costs and retirement savings plans to surface niche benefits most workers overlook entirely.

Running a yearly eligibility check before tax season helps you avoid missing smaller complementary credits alongside the Saver’s Credit, cutting long-term living expenses while building consistent retirement wealth on a limited hourly income.

Benefits.gov Federal All-in-One Benefit Matching Tool

FAQ Section

Q1: What is the maximum Saver’s Credit a single low-wage worker can receive in 2026?

A1: Single filers hitting the 50% tier can claim up to $2,000 for $4,000 in qualified retirement contributions within the tax year. Married joint filers can reach a combined maximum credit of $4,000 annually. This simple saver’s credit 2026 guide for low-wage hourly workers clearly lays out all tier maximums for every filing status.

Q2: Does receiving EITC make me ineligible to claim the Saver’s Credit?

A2: No. The two federal tax credits operate independently and stack fully together. Millions of low-income working families collect both refunds every filing season with no reduction to either payout amount.

Q3: Can part-time seasonal hourly workers qualify for the retirement savings credit?

A3: Yes. Any worker with valid W-2 earned income under the yearly AGI caps can claim the Saver’s Credit, regardless of full-time, part-time or seasonal employment status. Self-employed low earners also qualify with SEP IRA or SIMPLE IRA deposits.

Q4: Will claiming the Saver’s Credit raise my taxable income for future tax years?

A4: The Saver’s Credit counts as a refundable tax credit, not taxable gross income. Receiving this refund does not push you into higher tax brackets or lower your eligibility limits for federal benefit programs in subsequent fiscal years.

Q5: What documents do I need to complete Form 8880 successfully?

A5: Gather all yearly retirement account statements including 1099-R, 5498 and workplace 401(k) contribution summaries. Your W-2 wage forms confirm household AGI for tier placement calculations, and IRS Free File stores all submitted records securely for future tax returns. Refer back to this simple saver’s credit 2026 guide for low-wage hourly workers to double-check all required paperwork.

Conclusion

Simple Saver’s Credit 2026 guide for low-wage hourly workers unlocks a powerful, widely ignored IRS tax break built specifically for employees living on modest hourly pay. Tiered refund percentages return up to half of every dollar placed into approved retirement accounts, with a $2,000 yearly maximum credit for single filers.

Unlike restrictive high-income retirement tax advantages, this credit uses flexible income limits that fit minimum-wage staff, part-time caregivers and seasonal laborers across every US industry. The credit stacks seamlessly alongside EITC, LIHEAP and unclaimed federal cash assets without creating eligibility conflicts or benefit reductions.

All filing tools, official forms and eligibility verification portals listed in this article operate through free government .gov platforms, eliminating expensive private tax preparation fees for low-income households. Checking dormant unclaimed retirement balances annually further boosts your qualifying contribution total to maximize your yearly credit value.

Consistently small monthly IRA or workplace retirement deposits paired with the Saver’s Credit refund creates steady long-term retirement wealth, breaking the common myth that low hourly earnings make saving for old age impossible. Pair this IRS credit with intentional monthly budget cuts and federal cash benefit stacking to build both short-term emergency funds and lifelong retirement security.

Disclaimer

All federal benefit rules, income limits and grant amounts referenced in this article apply exclusively to the 2026 tax and fiscal year.

Policy adjustments may occur at state and federal levels after publication.

We are not licensed tax attorneys, CPAs or official government representatives.

All program eligibility verifications, tax filings and benefit applications must be completed via official .gov federal portals to confirm individual qualification.

This content is for general educational guidance only and does not constitute official financial, tax or legal advice.

Savelyfi and CalcfincePro accept no liability for financial outcomes resulting from reader self-submitted government benefit claims.