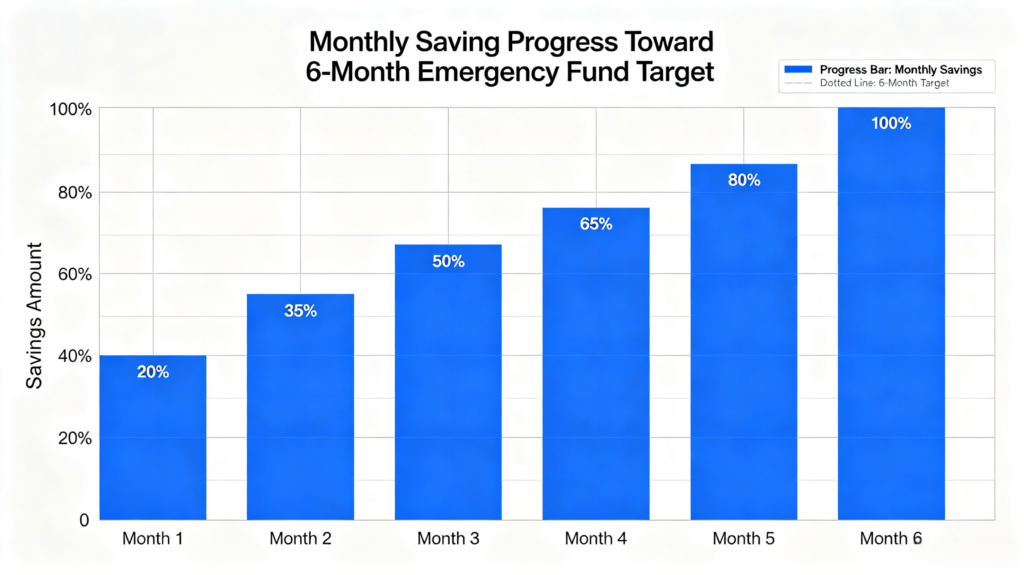

Learning how to build a 6 month emergency fund fast on low income helps regular workers avoid high-interest loans when unexpected bills pop up. Most low-earning households drain all cash on urgent medical fees or car repairs and fall into credit card debt without emergency savings.

Even if you barely have leftover money each paycheck, you can steadily build a 6 month emergency fund with small, regular deposits and simple spending tweaks. You do not need a huge salary to finish your safety reserve within 12 to 24 months.

What Makes a 6 Month Emergency Fund Critical for Low Earners

First of all, unexpected costs are the top reason low-income families go into debt. Job cuts, sudden sickness and vehicle breakdown can happen anytime, and a complete 6 month emergency fund covers all living costs without borrowing money.

Besides, this fund only covers essential needs such as rent, groceries and utilities, not casual shopping or travel. Separating emergency money from daily checking prevents accidental overspending of your safety cash.

Practical Steps to Build a 6 Month Emergency Fund Fast on Limited Pay

To start with, calculate your minimal monthly essential spending. Cut all non-essential subscriptions and takeout costs to lock down your baseline expense number for the fund target.

Next, open an independent high-yield savings account separate from your daily bank card. Automatic weekly transfers stop you from forgetting to save toward your 6 month emergency fund goal.

Quick tip: Calculate your exact savings target effortlessly with free financial tools at calcfincepro.com. Input monthly cost, expected saving cycle and get instant numbers for your 6-month emergency goal.

Lastly, add tiny side hustle earnings directly into emergency savings. Even $50 extra per week speeds up your saving timeline noticeably without affecting regular life quality.

Easy Spending Hacks to Speed Up Your Saving Progress

For one thing, swap expensive daily coffee and dining out for homemade meals. Small daily cuts add up quickly to feed your 6 month emergency fund steadily every single month.

For another, review existing monthly bills like internet and insurance. Negotiate lower rates with providers to free up extra cash for savings effortlessly.

In addition, put all unexpected windfalls including tax refunds and cash gifts straight into your emergency fund instead of impulsive shopping.

Common Saving Mistakes That Delay Emergency Fund Goals

In fact, many beginners pause saving once they hit small targets, which drags back finishing a full 6 month emergency fund. Keep fixed auto-transfer no matter how much you have already saved.

Moreover, another typical mistake is mixing emergency money with regular spending money. Once funds get merged, people easily spend reserved cash on unnecessary items.

Above all, never dip into emergency savings for non-urgent wants, as this habit will break your long-term saving schedule entirely.

In the end, stick to your fixed saving schedule month after month. Gradually you will fully complete your 6 month emergency fund and get rid of financial panic from sudden unexpected costs.

Related: zero based budget template: Stop Overspending 2026

Reference: FDIC official financial education page

Recommended Free Budget Calculator: CalcFinPro Online Financial Calculator