A reliable zero based budget template is the fastest solution for beginners who overspend monthly. Millions of regular workers waste hundreds of dollars on unnecessary purchases without noticing, and zero-based budgeting fixes this common money trouble by assigning every single dollar a clear spending job.

If you pay all bills but end up with zero savings at month-end, a ready-to-use zero based budget template can reorganize your cash flow within 30 minutes. Unlike loose 50/30/20 budgeting, this method requires income minus expenses equals zero, so no cash vanishes into unplanned impulse buys.

What Is Zero-Based Budgeting for New Budgeters?

First of all, the core logic of any practical zero based budget template is simple: every dollar of take-home pay gets allocated to needs, wants, savings or debt payoff before each new month. Unassigned cash no longer exists, so unexpected overspending cannot drain your bank balance easily.

This template splits your budget into four fixed buckets: essential monthly bills, daily leisure costs, emergency fund deposits, and high-interest debt payback. New budgeters avoid confusion, for every expense locks into its preset fund to cut random shopping temptations.

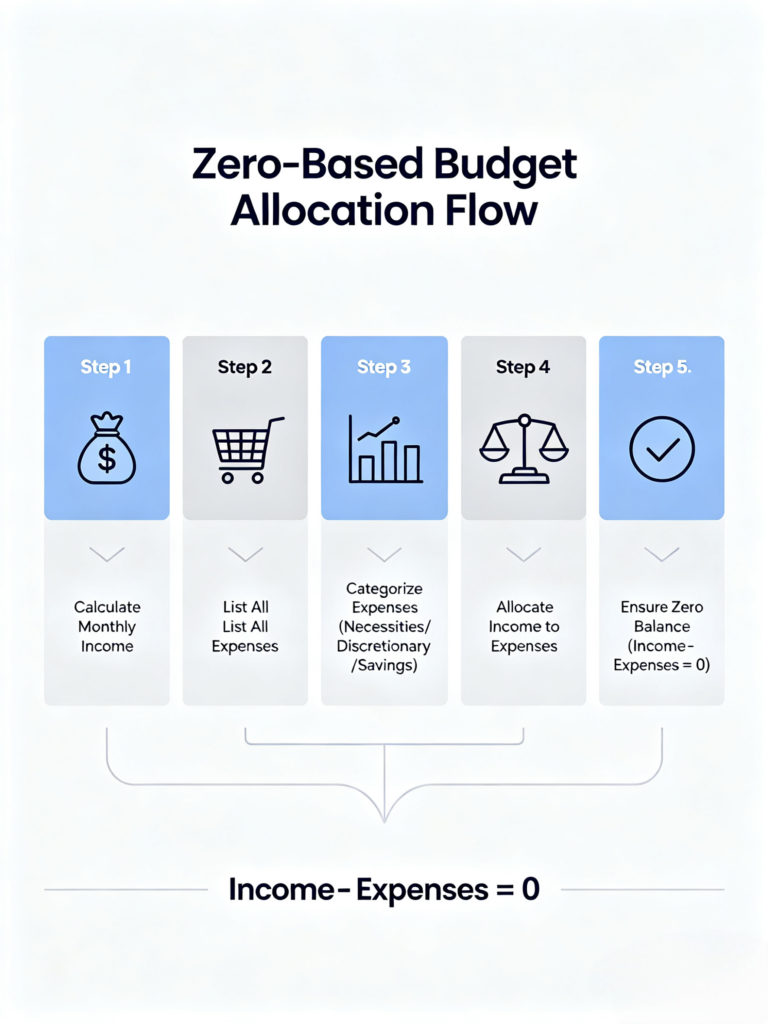

Quick Steps to Fill Your Zero Based Budget Template Correctly

To start with, calculate your exact monthly after-tax income from salary, side gigs and passive payouts. Note down the total amount at the top of this budgeting file to set your spending ceiling.

Next, list non-negotiable essential costs first: rent, utilities, grocery, auto fuel, health insurance and regular medication. Fill these fixed fees into the needs column to secure necessary spending.

Finally, split leftover money into three parts: leisure spending, regular savings and extra debt payment. Adjust each amount until total income matches all allocated costs to hit the zero-balance rule.

Core Benefits of Zero Based Budget Template Tool

For one thing, the first advantage is instant overspending control. Pre-set funds on this planner stop you from diverting rent or savings money to coffee and online shopping.

For another, consistent emergency savings grow without financial stress. Fixed saving slots push regular deposits each pay cycle, slowly building your 3-6 month emergency safety pool.

Besides, zero-based budgeting speeds high-interest debt paydown. Extra fund slots let spare cash go straight to credit card bills and cut costly monthly interest.

Common Beginner Budget Mistakes to Avoid

In fact, many new users fail budgeting because they skip updating their zero based budget template after pay raises or bill hikes. Revise category amounts once your income or regular expense shifts to keep data accurate.

Another frequent error is oversize discretionary funds, which still causes wasteful shopping. Keep your wants budget reasonable to stick to your pre-planned financial setup.

In the end, stick to your customized planner for two months. Uncontrolled overspending fades naturally, and your monthly savings will grow steadily with every paycheck.

Related: 50/30/20 Budget Rule: Beginner Step-by-Step Guide 2026

Reference: National Financial Educators Council Official Site