TL;DR

how to stop feeling hopeless about retirement savings at 45: Most low-income workers who hit 45 and carry minimal retirement balances sink into paralyzing hopelessness, fueled by unfair peer comparison, misunderstood compound interest rules, and zero knowledge of 2026 IRS catch-up contribution benefits. This actionable guide walks you through proven mindset shifts, official federal retirement policies, data-backed growth projections, and free age-aligned financial calculators that let late savers reliably close their savings gap without drastic cuts to daily living costs.

Why how to stop feeling hopeless about retirement savings at 45 Is The Top Financial Question For Mid-Career Low Earners

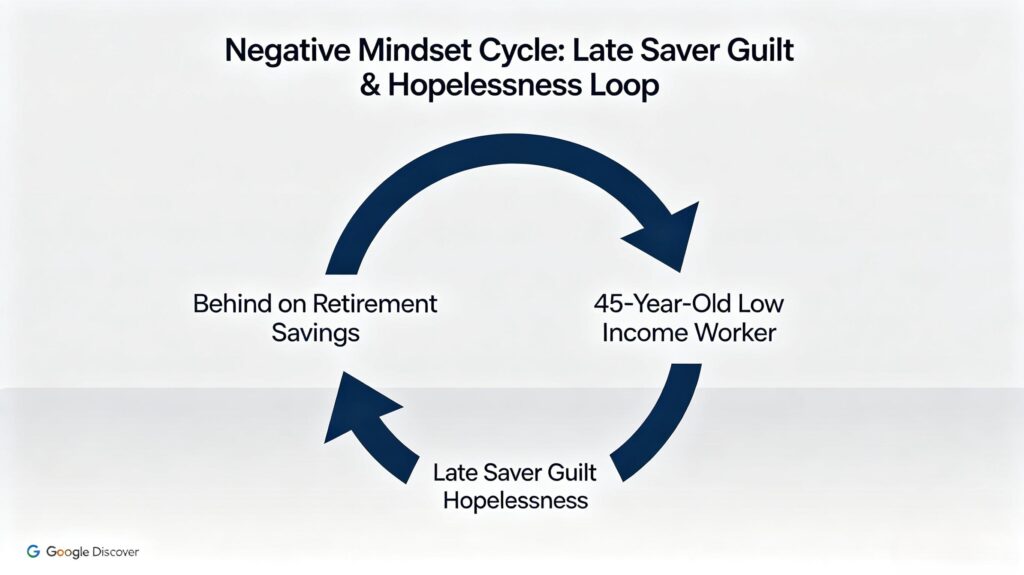

If you are 45 and stuck wondering how to stop feeling hopeless about retirement savings at 45, you belong to the largest group of overlooked late retirement savers across the U.S. Millions of hourly and low-salary Americans spend their 20s paying crippling student loan debt, renting cramped housing, and launching young families with no extra cash for long-term investing. Their 30s become consumed with childcare bills, rising grocery and utility inflation, and mortgage minimum payments that wipe out any potential monthly surplus for retirement accounts.

By the time their 45th birthday arrives, they log into their 401(k) or IRA platforms and stare at balances far below generic online savings benchmarks. This immediate shock triggers a self-sabotaging mental cycle that crushes every attempt to build consistent saving habits. You do not lack the ability to catch up; you lack accurate data and restructured thought patterns to beat hopelessness for good.

This toxic loop repeats for thousands of mid-career workers each year: you compare your tiny retirement balance to peers who started saving at 22, conclude you have missed your only shot at financial security, procrastinate all planning tasks, and overspend on instant gratification to mask feelings of failure. Breaking this cycle is the first critical step if you want to master how to stop feeling hopeless about retirement savings at 45.

The Unfair Peer Comparison Mindset That Worsens Hopelessness For 45-Year-Old Savers

The number one mental barrier stopping anyone learning how to stop feeling hopeless about retirement savings at 45 is constant, unbalanced comparison against early retirement savers. Online finance blogs and social media feed this harmful habit by highlighting investors who contributed steady sums throughout their twenties, ignoring the massive financial disadvantages young entry-level workers face.

People in their 20s only possess one financial advantage: time. They carry minimum wage or entry-level salaries, six-figure student debt burdens, and zero home equity to leverage for extra cash flow. The average 45-year-old low-income worker, by contrast, has reached their career’s peak earning bracket, eliminated most high-interest early-life debt, and seen children grow out of expensive full-time childcare expenses. This creates far larger monthly disposable income that can be directed straight to retirement contributions.

As Investopedia’s official late-retirement planning research confirms, mid-career savers hold unique catch-up strengths that twenty-something beginners cannot replicate. Larger regular deposits, stable long-term employment, and mature risk management all offset your shorter investment timeline.

Read Investopedia’s full guide to late retirement catch-up strategies

2026 IRS Catch-Up Contribution Rules To Eliminate Powerlessness For Late Savers

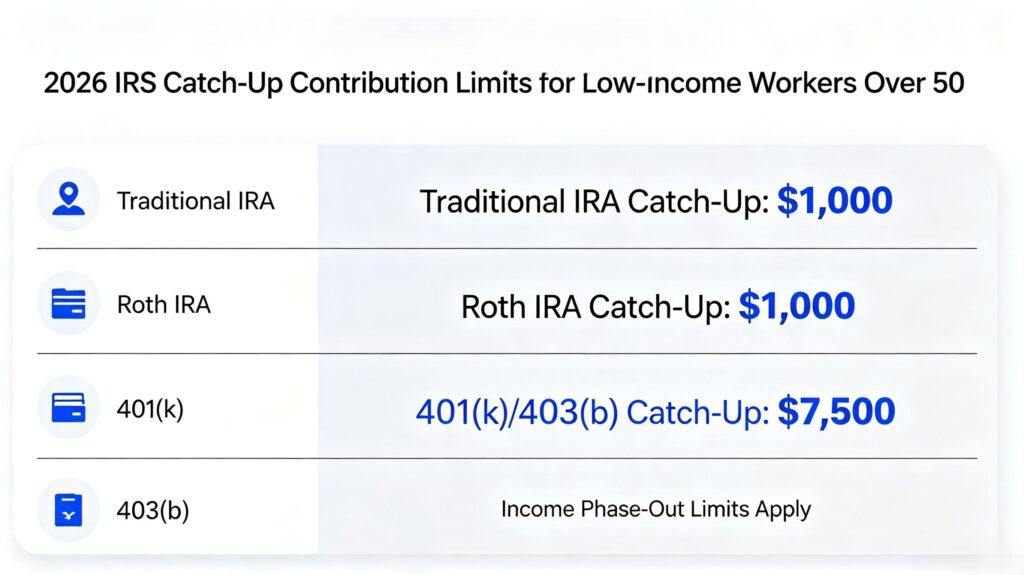

A core piece of solving how to stop feeling hopeless about retirement savings at 45 lies in mastering federal retirement rules created exclusively for workers who start saving late. Most 45-year-olds have no awareness of IRS catch-up contribution limits launching once they turn 50, which legally permit you to deposit thousands more into tax-advantaged retirement accounts every single year.

These special catch-up allowances exist specifically to reverse the “I’m too far behind” despair plaguing mid-career Americans. Once you cross age 50, you can exceed standard annual maximums for both 401(k) and IRA plans, rapidly shrinking your total savings gap over your remaining working years. Knowing these official legal rules erases the helpless mindset that makes you believe nothing can fix your underfunded retirement accounts.

Check official 2026 IRS catch-up contribution limits here

Instead of guessing random monthly savings targets, map your annual deposits around updated 2026 IRS catch-up figures. This structured, government-backed strategy delivers predictable, legal wealth growth without forcing you to slash essential household spending to unlivable levels.

Realistic SSA Social Security Expectations To Eliminate Extreme Retirement Panic

Many people researching how to stop feeling hopeless about retirement savings at 45 swing between two equally destructive false beliefs about Social Security benefits. One group assumes government payouts will fully cover every retirement expense and skips personal saving entirely. The other group writes off Social Security as useless and spirals into catastrophic financial anxiety with no baseline safety net in mind.

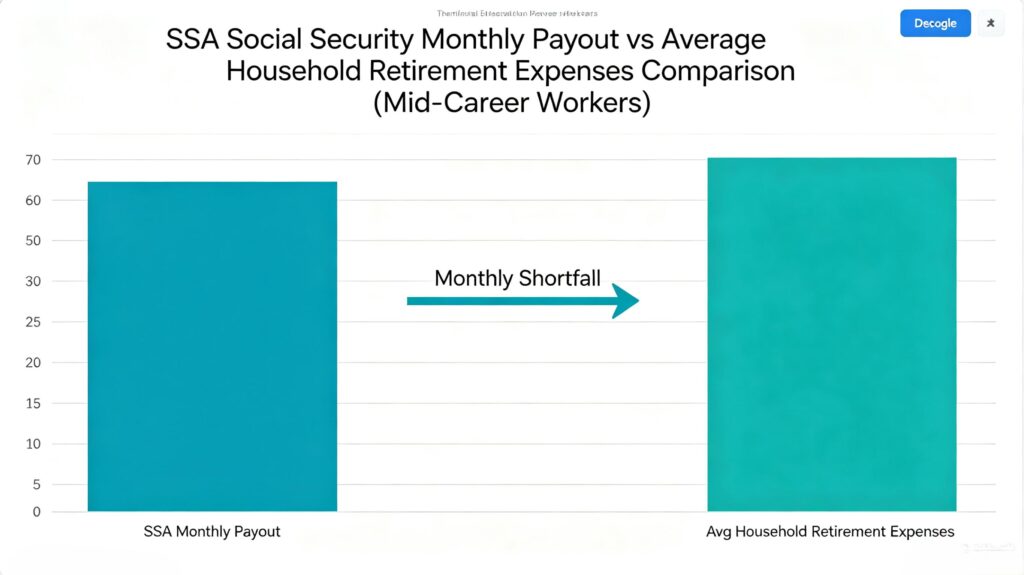

The Social Security Administration publishes transparent, updated national payout data every fiscal year that creates balanced, realistic expectations for every late saver. Official statistical analysis verifies standard Social Security monthly checks only cover roughly 40% of average low-to-middle-income household retirement living costs.

This single data point rewires your entire outlook on post-work finances. You no longer fear total poverty after leaving your job, nor do you rely solely on federal benefits and neglect personal investing. You gain a clear numerical target for how much private retirement savings you need to fill the remaining 60% of your future monthly bills, turning vague paralyzing fear into measurable saving goals.

View official SSA retirement benefit planning resources

Debunking The “Compound Interest Only Works For 30+ Years” Myth For 45-Year-Old Savers

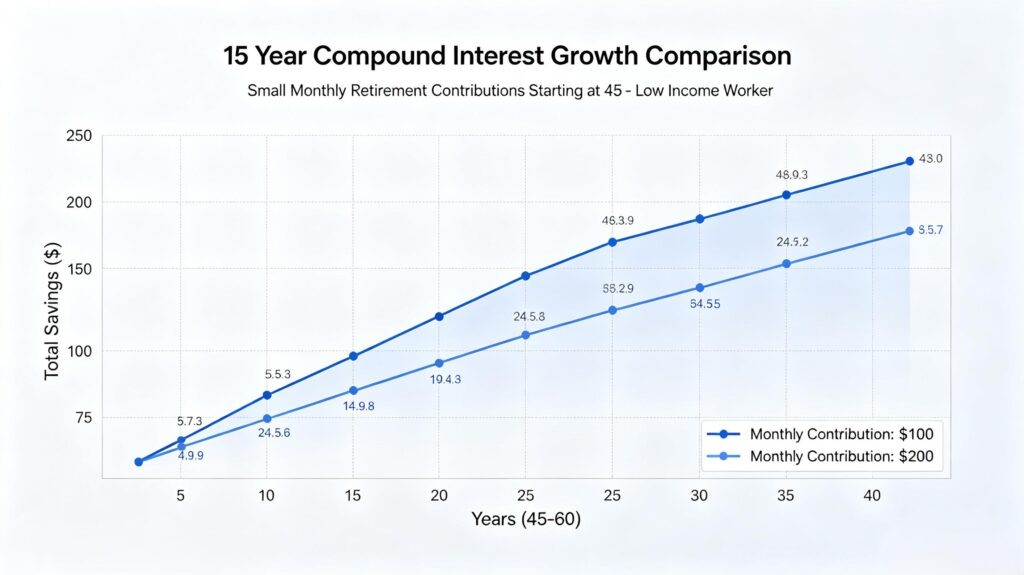

One pervasive false financial myth keeps thousands stuck on how to stop feeling hopeless about retirement savings at 45: the idea compound growth cannot generate meaningful wealth over a 15–20 year saving window. This misconception convinces mid-career workers their small monthly deposits are completely pointless, pushing them to abandon retirement planning indefinitely.

Compound interest functions exponentially regardless of how many years you invest, and your higher mid-life monthly contribution amounts amplify returns dramatically compared to tiny twenty-something deposits. Even modest consistent monthly contributions of $200–$500 grow into six-figure retirement balances before your full retirement age of 67. Once you turn 50 and add IRS catch-up deposits, your portfolio’s growth rate accelerates even faster.

The critical mindset shift here is abandoning all-or-nothing perfectionism. You do not need to max out your retirement accounts this month to make progress. Steady, small recurring contributions beat sporadic massive one-time deposits and total inaction every single time for late-start retirement portfolios.

Data-Driven Free Calculator Tools To Visualize Catch-Up Retirement Growth

To fully resolve how to stop feeling hopeless about retirement savings at 45, replace blind guessing with personalized, data-backed financial forecasting tools. Abstract, undefined saving targets sustain hopelessness, while visible, adjustable growth projections build long-term confidence and consistent motivation.

Our age-specific retirement savings planning guide breaks down tiered contribution benchmarks custom-built for workers in their 40s, 50s, and pre-retirement years, discarding generic saving rules written exclusively for people who began investing in their youth. This resource aligns every goal with your current low-income budget and remaining working timeline:

our complete age-based retirement savings planning guide

Complement your long-term planning framework with our free investment growth calculator, which lets you test custom monthly deposit sizes, average annual market return rates, and exact saving durations to generate a clear visual forecast of your future retirement balance. This tool eliminates all uncertainty around how extra catch-up deposits shorten your wealth-building timeline:

free investment growth calculator to model your catch-up savings trajectory

These two interconnected site tools transform vague financial hope into concrete, trackable progress, so you never again feel permanently stuck behind on retirement funding at age 45.

Four Core Permanent Mindset Shifts To Beat Retirement Hopelessness At 45

1. Ditch Peer Comparison And Track Only Personal Monthly Savings Progress

Stop measuring your total retirement account value against people who saved for 20 extra years before your mid-career stage. Focus solely on raising your own monthly contribution amount incrementally and trimming non-essential household waste. Your unique mid-life earning power creates an exclusive catch-up path no early starter can replicate.

2. Swap Vague Dread For Official IRS And SSA Data-Based Planning

Every time hopeless thoughts surface, reference the 2026 IRS catch-up contribution limits and SSA Social Security payout statistics laid out in this guide. Federal official guidelines eliminate financial uncertainty and hand you full control over shrinking your retirement savings gap year after year.

3. Abandon Perfectionist All-Or-Nothing Saving Standards

You are not required to hit maximum annual retirement contribution limits immediately to make meaningful progress. Tiny recurring monthly deposits compound steadily over 15–20 years, and partial consistent saving always delivers better long-term results than complete avoidance of retirement planning.

4. Fully Trust Short-Term Compound Growth Potential For Mid-Career Savers

15 to 20 years of disciplined regular investing generates substantial six-figure wealth for 45-year-old late starters. Consistent contributions through your remaining working decades create enough principal and compound returns to fund a stable, low-stress retirement lifestyle without relying entirely on government benefits.

Frequently Asked Questions About how to stop feeling hopeless about retirement savings at 45

Is it truly too late to fix my retirement savings if I start catching up at 45?

It is never too late to rebuild your retirement nest egg at 45, and learning how to stop feeling hopeless about retirement savings at 45 unlocks actionable catch-up strategies unavailable to younger low-income earners. Your higher mid-career income, upcoming IRS catch-up contribution eligibility after age 50, and 15–20 year compound growth window combine to create a fully viable path to secure post-work finances.

Why do I constantly feel hopeless looking at my retirement account at 45?

Persistent hopelessness stems from four overlapping mental traps: unfair comparison to early savers, misunderstanding short-term compound interest performance, lack of knowledge about federal catch-up retirement rules, and distorted over/under-estimation of Social Security monthly benefits. Each barrier can be dismantled with the data and mindset shifts covered throughout this article.

What monthly savings target should a low-income 45-year-old set to catch up on retirement?

Low-income workers aged 45 should start with sustainable small monthly contributions and increase deposits once turning 50 using IRS catch-up allowances. Input your exact income, current retirement balance, and target retirement age into our free investment growth calculator to generate a fully personalized monthly saving number tailored to your unique financial situation.

Final Closing Thoughts

Mastering how to stop feeling hopeless about retirement savings at 45 does not require massive side-hustle income spikes or risky high-yield speculative investments. The solution hinges on rewriting your harmful limiting financial mindsets, following verified IRS and SSA federal retirement policies, trusting proven compound interest growth over a 15–20 year timeline, and leveraging free data-driven planning calculators to rebuild your retirement outlook from scratch. At age 45, you still hold 15 to 20 high-earning investment years ahead of you, more than enough time to close your savings gap and eliminate lifelong post-retirement financial anxiety.

Disclaimer

This educational content about how to stop feeling hopeless about retirement savings at 45 serves general informational purposes only and does not constitute personalized certified financial planning advice. All 2026 IRS catch-up contribution figures, Social Security payout statistics, and compound growth projections act as reference examples. Consult a licensed fiduciary financial advisor to build customized retirement strategies aligned with your unique household income, outstanding debt, and long-term post-work lifestyle goals.