TL;DR

Will 2026 Social Security 2.8% COLA raise cover higher Medicare Part B premiums for low income retirees? For most low-income hourly and retired workers in the United States, the small 2.8% cost-of-living adjustment announced for 2026 will barely offset rising Medicare Part B costs, leaving many seniors with zero net gain or even less monthly take-home income. Low-income retirees face the toughest budget squeeze because they rely almost entirely on Social Security and have no extra savings to absorb federal healthcare premium hikes.

If you are approaching retirement or already receiving benefits, it is critical to calculate your net monthly gain after insurance costs. You can accurately forecast your future retirement budget using the free Retirement Savings Calculator to avoid unexpected shortfalls in your fixed monthly income.

Introduction: Why the 2026 COLA News Is Confusing for Low-Income Retirees

Every year, millions of American seniors wait anxiously for the official Social Security COLA announcement. A cost-of-living adjustment is supposed to help benefits keep up with rising consumer prices, housing costs, and medical inflation. For 2026, the Social Security Administration confirmed a 2.8% COLA increase, which sounds positive on the surface for fixed-income retirees.

However, low-income retirees quickly realize that headline benefit increases rarely translate to real money in their bank accounts. The biggest offset comes from rising Medicare Part B monthly premiums, which automatically deduct from Social Security checks for most enrolled seniors. Many low-wage workers who spent decades in hourly jobs now find their annual raise completely erased by federal healthcare cost increases.

According to official announcements released by the Social Security Administration, the 2026 COLA will apply to more than 75 million Americans receiving Social Security and Supplemental Security Income benefits (SSA, 2025) https://www.ssa.gov/news/en/press/releases/2025-10-24.html. While the percentage increase is fixed nationwide, the real financial impact varies drastically based on how much each household pays for Medicare coverage.

For low-income retirees who have no private retirement savings, no investment income, and no family financial support, even a small Medicare premium hike can create serious monthly budget pressure. Understanding exactly how the 2026 COLA interacts with Medicare costs allows seniors to adjust their spending habits and avoid living paycheck to paycheck during retirement.

What the Official 2026 Social Security 2.8% COLA Actually Means for Seniors

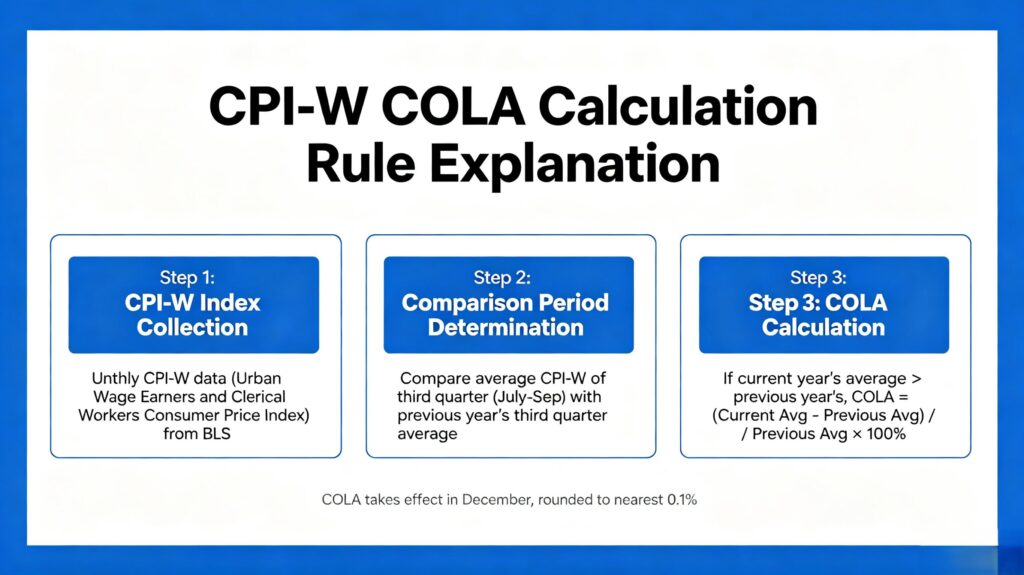

The 2.8% COLA for 2026 is calculated based on annual inflation data tracked by the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This official adjustment formula is designed to protect benefit recipients from losing purchasing power due to rising everyday costs(SSA, 2025) https://www.ssa.gov/cola/. On paper, every Social Security beneficiary receives a 2.8% increase in their monthly payment starting in January 2026.

For the average retired worker, the 2.8% raise equals approximately $56 extra per month in Social Security benefits. This amount varies slightly based on lifetime earnings records, benefit claiming age, and disability status. Higher earners receive larger absolute dollar increases, while low-income retirees receive smaller raw dollar gains despite facing identical Medicare premium increases.

This uneven dynamic creates a hidden poverty penalty for low-income seniors. Wealthier retirees with pensions, investment dividends, or savings can easily absorb higher Medicare costs. Low-income hourly workers who rely solely on Social Security have no financial buffer, meaning their entire COLA raise can disappear overnight due to federal healthcare deductions.

Many low-income retirees make the mistake of planning their 2026 budget based on the gross COLA increase instead of the net income after Medicare deductions. This common error leads to overspending, unexpected monthly deficits, and forced cuts to essential needs like groceries, utilities, and prescription medications.

2026 Medicare Part B Premium Increases That Offset Social Security Raises

While Social Security benefits are rising by 2.8% in 2026, Medicare Part B premiums are also increasing significantly for the upcoming year. Medicare Part B covers outpatient medical services, doctor visits, preventive care, and durable medical equipment, and it is mandatory for most retirees enrolled in traditional Medicare.

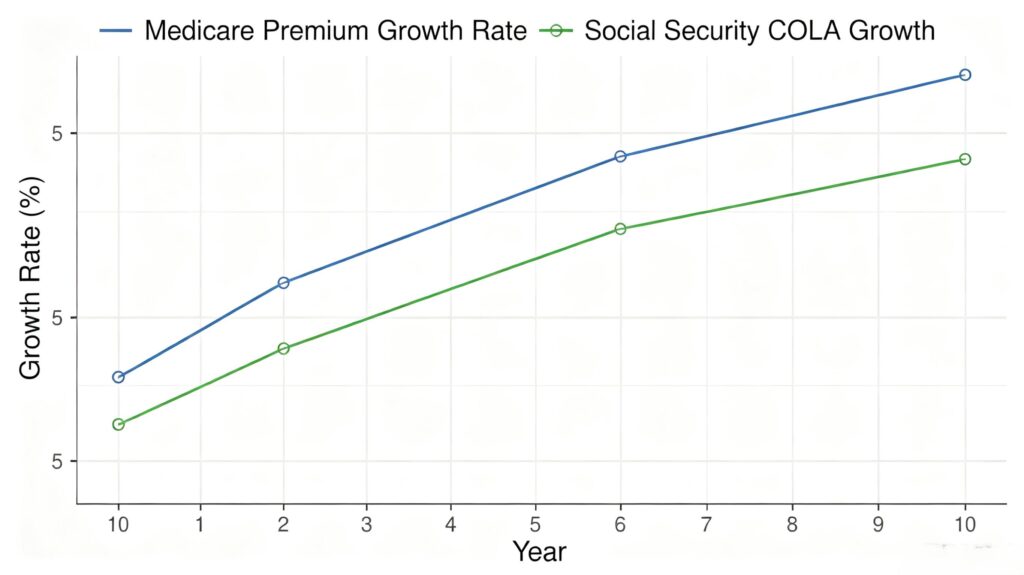

Financial analysts tracking federal retirement policy explain that Medicare premium inflation consistently outpaces Social Security COLA growth in most years, creating a gradual erosion of senior purchasing power (Investopedia, 2025) https://www.investopedia.com/social-security-cola-boosted-benefits-for-retirees-this-year-but-medicare-b-premium-threatens-to-cancel-the-gain-11851994. The 2026 pricing structure continues this long-term trend, putting disproportionate financial pressure on low-income households.

For standard Medicare Part B enrollees, the monthly premium increase directly reduces net Social Security income. Unlike income-tax brackets or benefit tiers that adjust for low-income status, standard Medicare premiums apply uniformly to most beneficiaries. Retirees with limited resources have no way to avoid these automatic deductions unless they qualify for special low-income subsidy programs.

Industry experts at senior financial advocacy organizations confirm that 2026 represents one of the largest gaps in recent years between COLA gains and Medicare cost growth (NSSA, 2025) https://www.nssapros.com/blog/2026-medicare-cost-increases. For millions of low-wage retirees, the math results in zero net financial improvement despite the official benefit increase announcement.

Real Math: Do Low-Income Retirees Actually Gain Money in 2026?

To understand the real impact of 2026 policy changes, low-income retirees must calculate gross COLA gains minus new Medicare premium costs. For the average low-benefit recipient, the 2.8% Social Security raise adds roughly $55 to $58 each month before deductions. After applying the updated 2026 Medicare Part B premium rates, most seniors see nearly all of that increase eliminated.

In many borderline low-income cases, the Medicare premium increase consumes the entire COLA adjustment, leaving no extra money for rising grocery prices, utility bills, or transportation costs. Some seniors even experience a slight net decrease in take-home Social Security income when additional healthcare-related fees and adjustments are included.

Senior financial education platforms specializing in budget assistance for retired hourly workers warn that this hidden net loss creates serious financial stress for vulnerable households (Senior Simple, 2025) https://www.seniorsimple.org/articles/medicare-part-b-premium-increase-2026. Many low-income retirees rely on every dollar of their Social Security check to cover basic survival expenses.

The biggest disadvantage falls on workers who spent their entire careers in low-wage hourly positions. These individuals never had enough disposable income to build large retirement savings or investment portfolios. Unlike higher-income professionals who can offset rising healthcare costs with passive income, low-income retirees depend entirely on federal benefit programs.

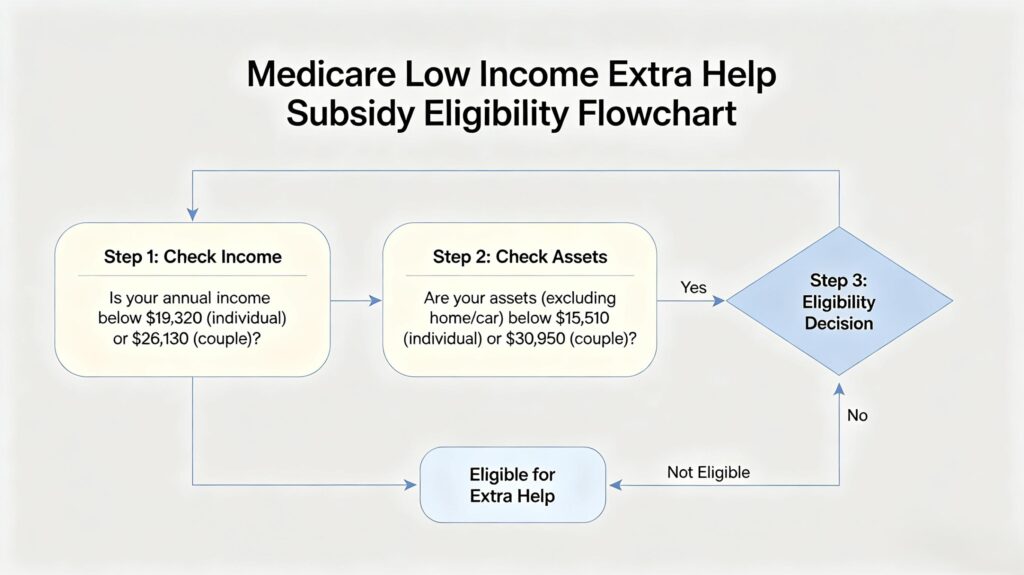

Low-Income Medicare Subsidy Programs That Can Save Your 2026 Budget

Although standard Medicare Part B premiums are rising in 2026, low-income retirees qualify for special federal subsidy programs designed to reduce or eliminate premium costs. These extra help benefits exist specifically to prevent benefit erosion for fixed-income seniors with limited financial resources.

The Medicare Part D Low-Income Subsidy and state-level Medicare savings programs provide premium assistance, deductible waivers, and cost-sharing reductions for eligible low-benefit recipients(NCOA, 2025) https://www.ncoa.org/article/part-d-low-income-subsidy-extra-help-eligibility-and-coverage-chart/. Many retirees do not realize they qualify for these programs and continue paying full Medicare premiums unnecessarily.

Eligibility guidelines are based on monthly Social Security income, total household resources, and state residency status. Seniors below specific income thresholds can receive full or partial premium coverage, which completely reverses the negative impact of 2026 Medicare hikes and preserves their COLA raise.

Legal and financial policy experts emphasize that low-income retirees should review their subsidy eligibility every year, especially during major benefit adjustment years like 2026 (Legal Clarity, 2025) https://legalclarity.org/social-security-updates-cola-benefits-and-limits/. Small changes in income, household status, or local assistance programs can open new savings opportunities for seniors.

How Low-Income Retirees Can Protect Their 2026 Retirement Budget

Understanding the gap between COLA increases and Medicare inflation allows seniors to implement practical budget adjustments for 2026 and beyond. The most effective strategies focus on reducing unnecessary expenses, maximizing subsidy eligibility, and planning long-term retirement finances wisely.

First, all retirees should verify their current Medicare plan and confirm whether they qualify for low-income premium relief. Applying for subsidies can instantly restore the full value of the 2.8% COLA raise and prevent monthly income loss. Many eligible seniors skip this step simply due to lack of awareness.

Second, retirees should review their overall retirement savings strategy to build protection against future healthcare inflation. Even small monthly savings during pre-retirement years can create a buffer against rising federal insurance costs. Learning how to plan your retirement savings at any age helps low-income workers avoid budget shocks during policy adjustment years.

Third, seniors should adjust their monthly spending to account for slower net income growth. Since COLA gains no longer fully match real-world inflation and healthcare costs, conservative budgeting prevents debt accumulation and financial instability during retirement.

Frequently Asked Questions

Will the 2026 2.8% Social Security COLA fully cover Medicare premium increases for low-income retirees?

In most standard cases, the 2.8% COLA raise does not fully cover rising 2026 Medicare Part B premiums for low-income retirees. The net monthly gain is minimal or zero for seniors paying standard premium rates, though low-income subsidy programs can eliminate this financial loss entirely for eligible households.

Why do Medicare premiums rise faster than Social Security COLA adjustments?

Medicare healthcare inflation follows medical industry cost trends, while COLA adjustments follow general consumer inflation data. Healthcare costs consistently outpace regular inflation, creating a persistent gap that disproportionately harms fixed-income low-wage retirees with no alternative income sources.

How can low-income seniors keep their full COLA raise in 2026?

Low-income seniors can retain their full 2026 COLA benefit by applying for federal Medicare low-income subsidies, reviewing their insurance plan annually, and maintaining a strict retirement budget that accounts for ongoing healthcare inflation.

Final Thoughts

The 2026 Social Security 2.8% COLA adjustment offers nominal relief for retired workers, but rising Medicare Part B premiums significantly reduce real take-home income for low-income seniors. For decades of hourly workers relying solely on federal benefits, this policy dynamic creates serious budget pressure that most ordinary financial advice ignores.

By understanding the official numbers, verifying subsidy eligibility, and planning long-term retirement finances carefully, low-income retirees can protect their monthly income and avoid losing their annual cost-of-living raise to healthcare inflation. Consistent small adjustments and proper tool usage make retirement stability achievable even on fixed low benefits.

Disclaimer: This article is for educational financial guidance only. All policy details, premium rates, and benefit adjustments are subject to official federal updates from SSA and CMS. Readers should verify current official rules before making final retirement budget decisions.